Author: Ben Thompson

Go to Source

The Harvard

Business Review Entrepreneur's Handbook: Everything You Need to Launch

and Grow Your New Business

Free $0.00 Amazon

It’s the refunds that blow my mind.

You may be surprised to know that, despite the fact I live in Taiwan, I have an Amazon Prime account. It turns out that Amazon ships to Taiwan, which is particularly useful if you need something rather obscure and you’re not quite sure where to buy it locally:

Amazon doesn’t simply make buying thing easy from the other side of the world, they make dealing with shipping and customs trivial; they do it all, and refund me if they over-estimated the cost. It’s so easy that it is easy to forget how much work went into making this possible. Moreover, the company isn’t standing still:

The only thing more surprising than this new benefit that arrived completely out of the blue is that there is a part of me that wasn’t surprised; for customers Amazon just keeps getting better, and why not add free shipping to Taiwan? Indeed, I expect the minimum price to decrease over time, which is my way of explaining why so many stories about Amazon — including, I guess, this one — start with the fact that relentless.com redirects to Amazon.com.

What is clear, though, is that any attempt to understand the relentlessness of the company redirects to their founder, Jeff Bezos, who announced plans to step down as CEO after leading the company for twenty-seven years. He is arguably the greatest CEO in tech history, in large part because he created three massive businesses, all of which generate enormous consumer surplus and enjoy impregnable moats: Amazon.com, AWS, and the Amazon platform (this is a grab-all term for the Amazon Marketplace and Fulfillment offerings; it is lumped in with Amazon.com in the company’s reporting). These three businesses are the result of Bezos’ rare combination of strategic thinking, boldness, and drive, and the real world manifestations of Amazon’s three most important tactics: leverage the Internet, win with scale, and being your first best — but not only — customer.

Amazon.com and Leveraging the Internet

While the mythology of founders centers around a tortured genius solving a problem for themselves and only then discovering product-market fit, Bezos started with the solution and then looked for a problem. That solution, broadly considered was the Internet, and more specifically “the everything store”, a concept that crystallized in discussions Bezos had with David Shaw, the founder of the eponymous hedge fund where he worked. The problem was how to start, and Bezos settled on books; he explained in a speech at Lake Forest College in 1998:

In the spring of 94 web usage was growing at 2300% a year. You have to keep in mind human beings aren’t good at understanding exponential growth; it’s just not something we see in our everyday life. But things don’t grow this fast outside of Petri dishes. It just doesn’t happen. When I saw this, I said, okay, what’s a business plan that might make sense in the context of that growth. I made a list of 20 different products that you might be able to sell online. I was looking for the first best product, and I chose books for lots of different reasons, but one primary reason. And that is that there are more items in the book space than there are items in any other category by far. There are over 3 million different books worldwide in all languages. The number two product category in that regard is music, and there are about 300,000 active music CDs. And when you have this huge catalog of products, you can build something online that you just can’t build any other way. The largest physical bookstores, the largest superstores, and these are huge stores, often converted from bowling alleys and movie theaters, can only carry about 175,000 titles. There are only a few that large. In our online catalog, we’re able to list over two and a half million different titles and give people access to those titles.

Being able to do something online that you can’t do in any other way is important. It’s all about the fundamental tenant of building any business, which is creating a value proposition for the customer, and online, especially three years ago, but even today and for the next several years, the value proposition that you have to build for customers is incredibly large. That’s because the web is a pain to use today! We’ve all experienced the modem hangups and the browsers crash — there are all sorts of inconveniences: websites are slow, modem speeds are slow. So if you’re going to get people to use a website in today’s environment, you have to offer them overwhelming compensation for this primitive infant technology. And I would claim that that compensation has to be so strong that it’s basically the same as saying, you can only do things online today that simply can’t be done any other way. And that’s why this huge number of products looked like a winning combination online. There’s no other way to have a two-and-a-half-million-title bookstore. You can’t do it in a physical store, but you also can’t do it in a print catalog. If you were to print the M’s on a card catalog, it would be the size of more than 40 New York city phone books.

What is so impressive about this formulation — in which, humorously, Bezos dramatically understated the Internet’s growth rate of 230000%, not 2300% (exponents are hard!) — is the way in which Bezos grasped both the opportunities and the pitfalls the Internet presented a new business, and took them to their logical conclusion. This sort of strategic thinking, in which Bezos didn’t simply understand a particular point of business but also its implications both now and in the future, was how Bezos transformed Amazon into a true tech company.

AWS and Tech Economics

That Amazon was even considered a tech company, at least for its first decade, was in many respects an accident of timing: there simply weren’t very many online businesses when Bezos got started, so anyone with a website was a tech company. The truth, though, is that Amazon was very much a retailer, with a bunch of managers it recruited from Walmart, and, after the dot-com bubble burst, under tremendous pressure to raise prices in the pursuit of profitability.

The turning point came in two parts. The first was a meeting Bezos had with Costco founder Jim Sinegal in 2001; from Brad Stone’s The Everything Store:

Sinegal explained the Costco model to Bezos: it was all about customer loyalty…”The membership fee is a onetime pain, but it’s reinforced every time customers walk in and see forty-seven-inch televisions that are two hundred dollars less than anyplace else,” Sinegal said. “It reinforces the value of the concept. Customers know they will find really cheap stuff at Costco.” Costco’s low prices generated heavy sales volume, and the company then used its significant size to demand the best possible deals from suppliers and raise its per-unit gross profit dollars.

Bezos immediately cut prices, but Sinegal’s core insight only truly crystallized later that year at an offsite with (soon-to-be-published) Good to Great author Jim Collins:

Drawing on Collins’s concept of a flywheel, or self-reinforcing loop, Bezos and his lieutenants sketched their own virtuous cycle, which they believed powered their business. It went something like this: Lower prices led to more customer visits. More customers increased the volume of sales and attracted more commission-paying third-party seller to the site. That allowed Amazon to get more out of fixed costs like the fulfillment centers and the servers needed to run the website. This greater efficiency then enabled it to lower prices further. Feed any part of this flywheel, they reasoned, and it should accelerate the loop.

Thus was the famous Bezos napkin diagram born:

This insight is what transformed Amazon from a retailer that leveraged the Internet to a tech company masquerading as a retailer. What is fascinating about this transition, though, is that AWS was still several years down the road; Amazon still looked like a retailer! The difference is that just as Bezos had started with a solution (the Internet) looking for a problem (books), in this case Bezos started with tech economics and applied them to retail.

The first tech CEO to truly grasp how tech economics were different from most other businesses was Bob Noyce (the future Intel founder) at Fairchild Semiconductor. From Michael Malone in The Intel Trinity:

In the spring of 1965…Noyce got up before a major industry conference and in one fell swoop destroyed the entire pricing structure of the electronics industry. Noyce may have had trouble deciding between conflicting claims of his own subordinates, but when it came to technology and competitors, he was one of the most ferocious risk takers in high-tech history. And this was one of his first great moves. The audience at the conference audibly gasped when Noyce announced that Fairchild would henceforth price all of its major integrated circuit products at one dollar. This was not only a fraction of the standard industry price for these chips, but it was also less than it cost Fairchild to make them.

The reason this was possible is that the true cost of integrated circuits came from the R&D costs to design them, and capital costs to manufacture them; the actual materials cost was practically zero. This meant that the best route to profitability was to make it up in volume. This equation is even more powerful in software, which has only R&D costs, and zero material costs. This overall concept, that tech is governed by a world of zero marginal costs, is what makes tech economics fundamentally different from most businesses.

Bezos, though, had one big problem: Amazon had to actually pay for the products it sold! To effectively pursue a tech economics strategy, i.e. bet everything on volume in an attempt to gain leverage on huge fixed costs, was exceptionally risky in an arena with inescapable marginal costs. Bezos, though, prioritized boldness; he wrote in his famous 1997 Letter to Shareholders that he would attach to every subsequent letter:

We will make bold rather than timid investment decisions where we see a sufficient probability of gaining market leadership advantages. Some of these investments will pay off, others will not, and we will have learned another valuable lesson in either case.

This was the exact approach Bezos took to the initial launch of AWS; from The Everything Store:

Bezos wanted AWS to be a utility with discount rates, even if that meant losing money in the short term. Willem van Biljon…proposed pricing EC2 instances at fifteen cents an hour, a rate that he believed would allow the company to break even on the service. In an S Team meeting before EC2 launched, Bezos unilaterally revised that to ten cents. “You realize you could lose money on that for a long time,” van Viljon told him. “Great,” Bezos said.

A decade later Amazon would finally break out AWS in its reporting and it was an absolute juggernaut; I called it The AWS IPO:

This is why Amazon’s latest earnings were such a big deal: for the first time the company broke out AWS into its own line item, revealing not just its revenue (which could be teased out previously) but also its profitability. And, to many people’s surprise, and despite all the price cuts, AWS is very profitable: $265 million in profit on $1.57 billion in sales last quarter alone, for an impressive (for Amazon!) 17% net margin.

Fast forward to Q4 2020, where AWS just reported $3.6 billion in profit on $12.7 billion in revenue; perhaps more tellingly in terms of Amazon’s transformation into a tech company, it is Andy Jassy, the longtime head of AWS, who is succeeding Bezos (yet still, reflecting Amazon’s business-centric roots, Jassy is an MBA, not an engineer).

Amazon’s Platform and the First Best Customer

AWS was not, as urban legend has it, borne out of the desire to utilize holiday capacity; after all, it is not as if Amazon kicked off AWS customers every Christmas! In fact, it took years for Amazon.com to fully run on AWS. AWS, though, was created to solve the internal problems that Amazon.com presented: how to create new customer experiences without constantly waiting for the infrastructure team to set up dedicated capacity.

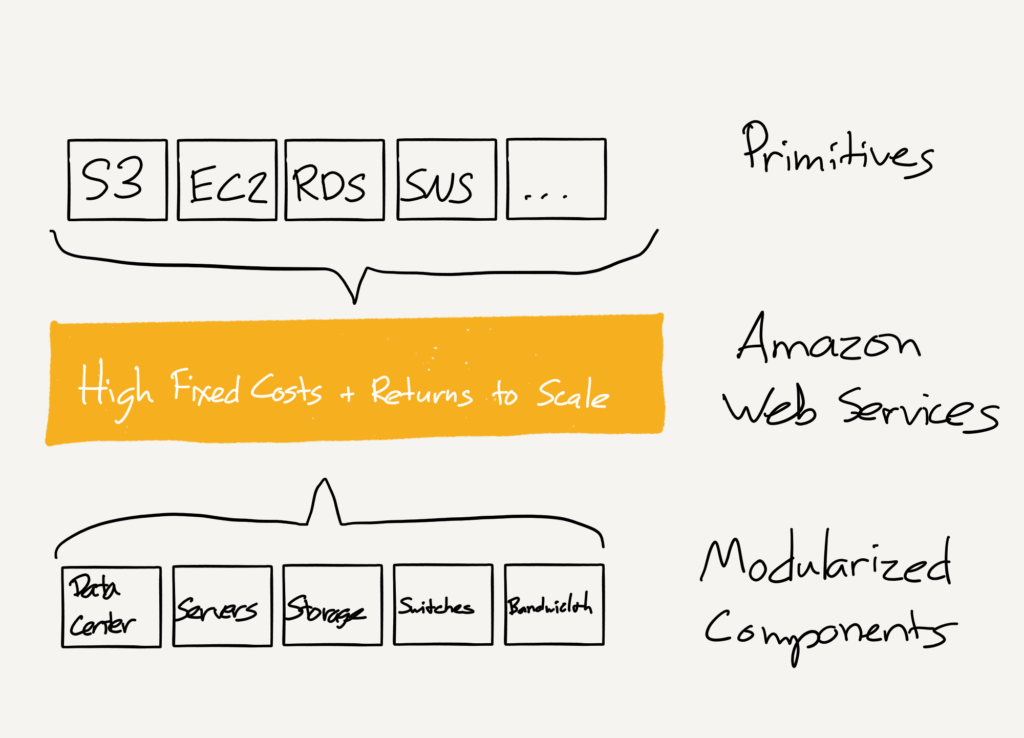

The solution was primitives: instead of building monolithic applications, Amazon’s infrastructure team should build basic compute offerings — like the EC2 instances above — so that their developers could make anything they wanted to. And then, having solved the problem for itself, Amazon could solve it for everyone. From The Amazon Tax:

The “primitives” model modularized Amazon’s infrastructure, effectively transforming raw data center components into storage, computing, databases, etc. which could be used on an ad-hoc basis not only by Amazon’s internal teams but also outside developers:

This AWS layer in the middle has several key characteristics:

- AWS has massive fixed costs but benefits tremendously from economies of scale.

- The cost to build AWS was justified because the first and best customer is Amazon’s e-commerce business.

- AWS’s focus on “primitives” meant it could be sold as-is to developers beyond Amazon, increasing the returns to scale and, by extension, deepening AWS’ moat.

This last point was a win-win: developers would have access to enterprise-level computing resources with zero up-front investment; Amazon, meanwhile, would get that much more scale for a set of products for which they would be the first and best customer.

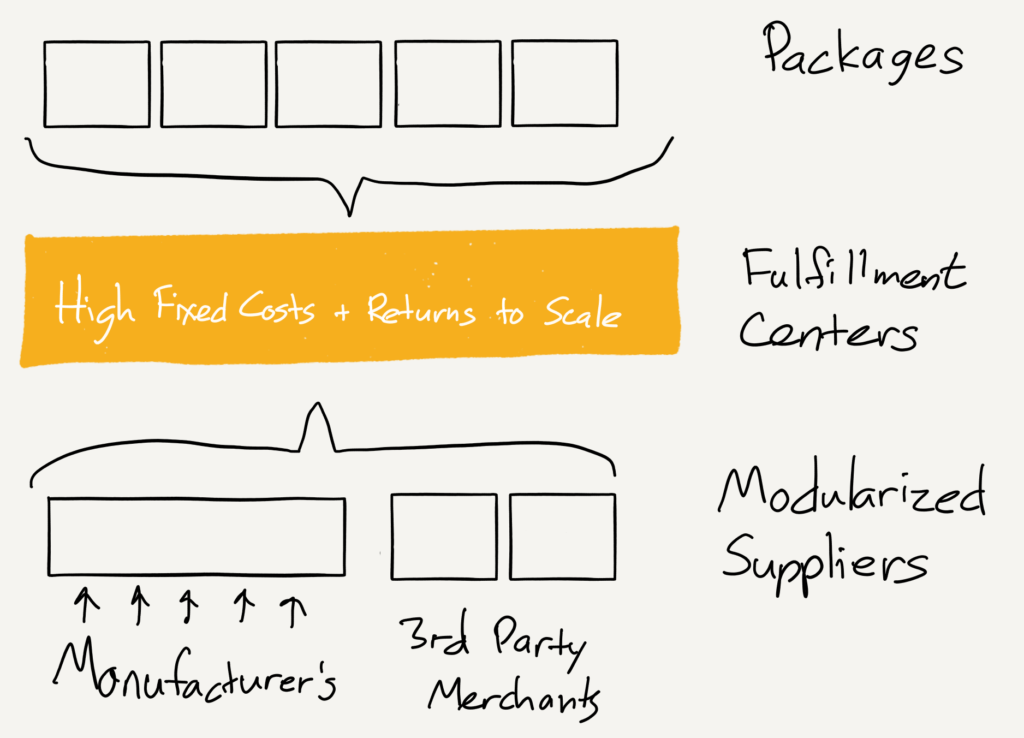

As I noted in that article, this exact same approach increasingly applied to the e-commerce side of the business:

Prime is a super experience with superior prices and superior selection, and it too feeds into a scale play. The result is a business that looks like this:

That is, of course, the same structure as AWS — and it shares similar characteristics:

- E-commerce distribution has massive fixed costs but benefits tremendously from economies of scale.

- The cost to build-out Amazon’s fulfillment centers was justified because the first and best customer is Amazon’s e-commerce business.

- That last bullet point may seem odd, but in fact 40% of Amazon’s sales (on a unit basis) are sold by 3rd-party merchants; most of these merchants leverage Fulfilled-by-Amazon, which means their goods are stored in Amazon’s fulfillment centers and covered by Prime. This increases the return to scale for Amazon’s fulfillment centers, increases the value of Prime, and deepens Amazon’s moat.

Over the last five years Amazon’s investment in fulfillment has ballooned into a multitude of new distribution centers, sortation centers, an Air Hub for Amazon’s growing fleet of airplanes, trucking, and a massive delivery operation that largely bypasses UPS and Fedex (while leveraging USPS for far-flung deliveries). At the same time the number of products sold by third-party merchants is now over 50% on a unit basis, and last quarter third-party seller services — where Amazon charges a merchant to stock and ship their goods — accounted for $27.3 billion in revenue.

Relentlessness and the Real World

This transformation in one respect brings the Bezos story full circle: the vision was an “Everything Store” — something that could only exist on the Internet — and while books were the best place to begin, they were only that — a beginning. Thanks in large part to Amazon’s platform the company has achieved Bezos’s vision.

What is somewhat ironic, though, is that while the Internet is unquestionably a critical component of what makes Amazon Amazon, what makes the company so valuable and seemingly impregnable is the way it has integrated backwards into the world of atoms. Real moats are built with real dollars, and Bezos has been relentless in pushing the company to continually invest in solving problems with real world costs, from delivery trucks to data centers and everything in-between. This application of tech economics to the real world is what sets Bezos apart.

The world, particularly the United States, has been a massive beneficiary, especially in 2020: when people were stuck at home, what was the company they depended on more than any other to deliver supplies? When companies had to go remote overnight, what was the infrastructure that made that possible? When time needed to be filled with entertainment, games, or video calls, where did those services run? The answer in all cases was Amazon, and the companies that rose up to compete with it. That is one heck of a crowning achievement for a career that changed the industry and the world.