Author: Benedict Evans

Go to Source

The Harvard

Business Review Entrepreneur's Handbook: Everything You Need to Launch

and Grow Your New Business

Free $0.00 Amazon

View fullsize

{kind=link}

View fullsize

{kind=link}

View fullsize

{kind=link}

View fullsize

We’ve been arguing about Apple’s app store rules for a decade now, but whatever your opinion of them, it should now be clear that something is going to change. The US has proposed two bills to regulate it (one mostly sensible, one not, as I wrote here), the UK is digging in, and the EU has already decided that the current situation is unacceptable. This prompts three questions:

-

How much money are we talking about?

-

What would a new situation look like?

-

And, who cares?

First, the numbers. Apple says it paid $45bn to developers in 2020, and hence total consumer billings were around $60bn and Apple’s commission around $15bn*. This is around 6% of Apple’s revenue. (It was also roughly the same as the entire global music industry’s revenue from digital. Remember when Apple was the iPod company?)

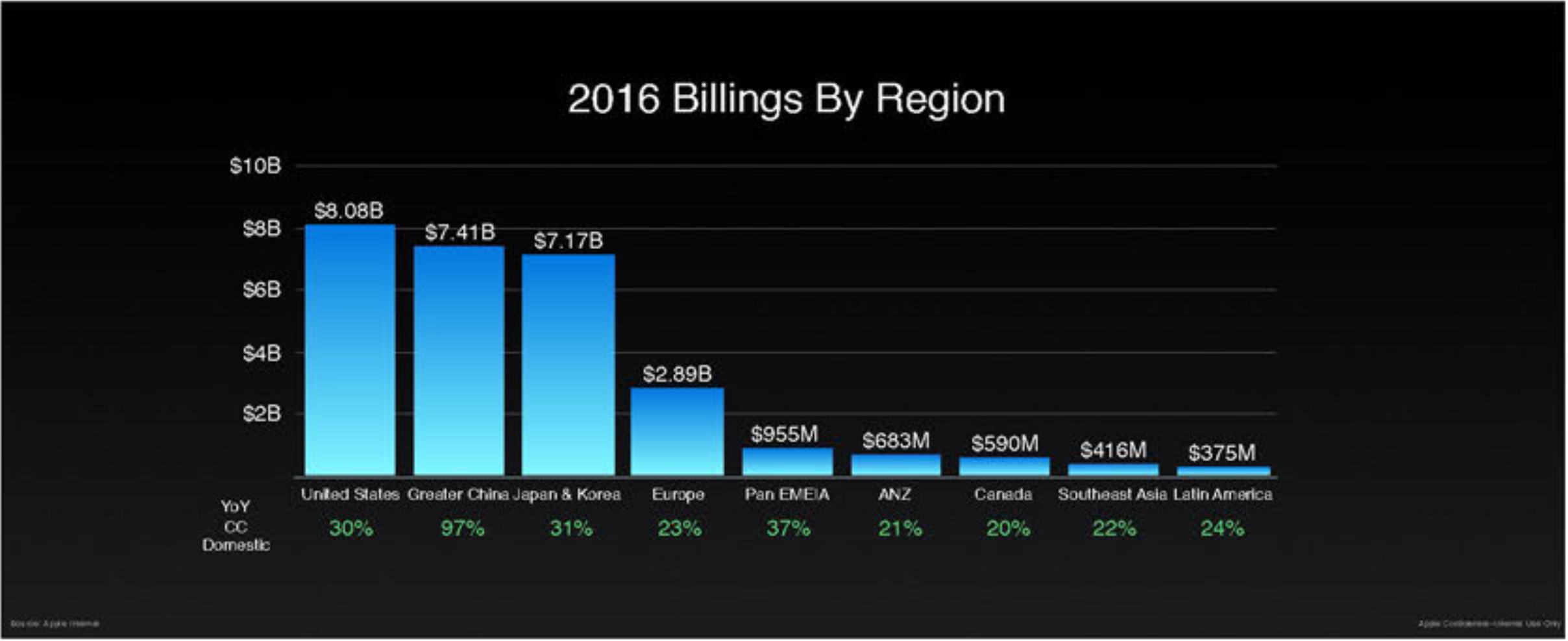

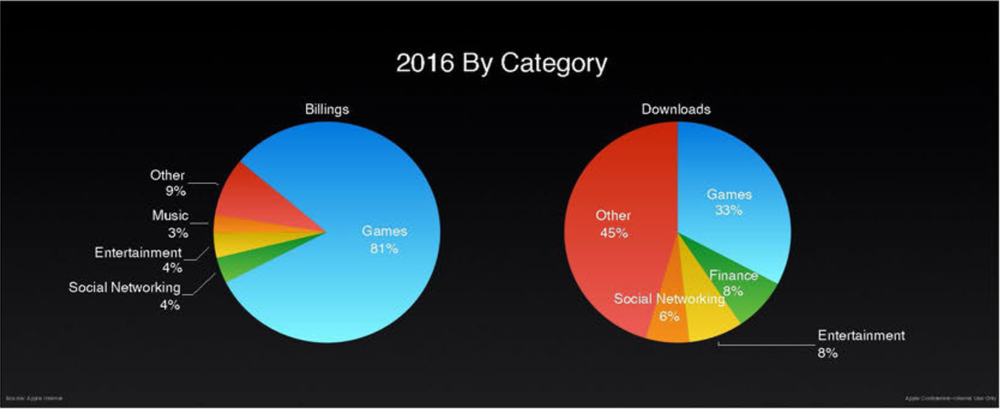

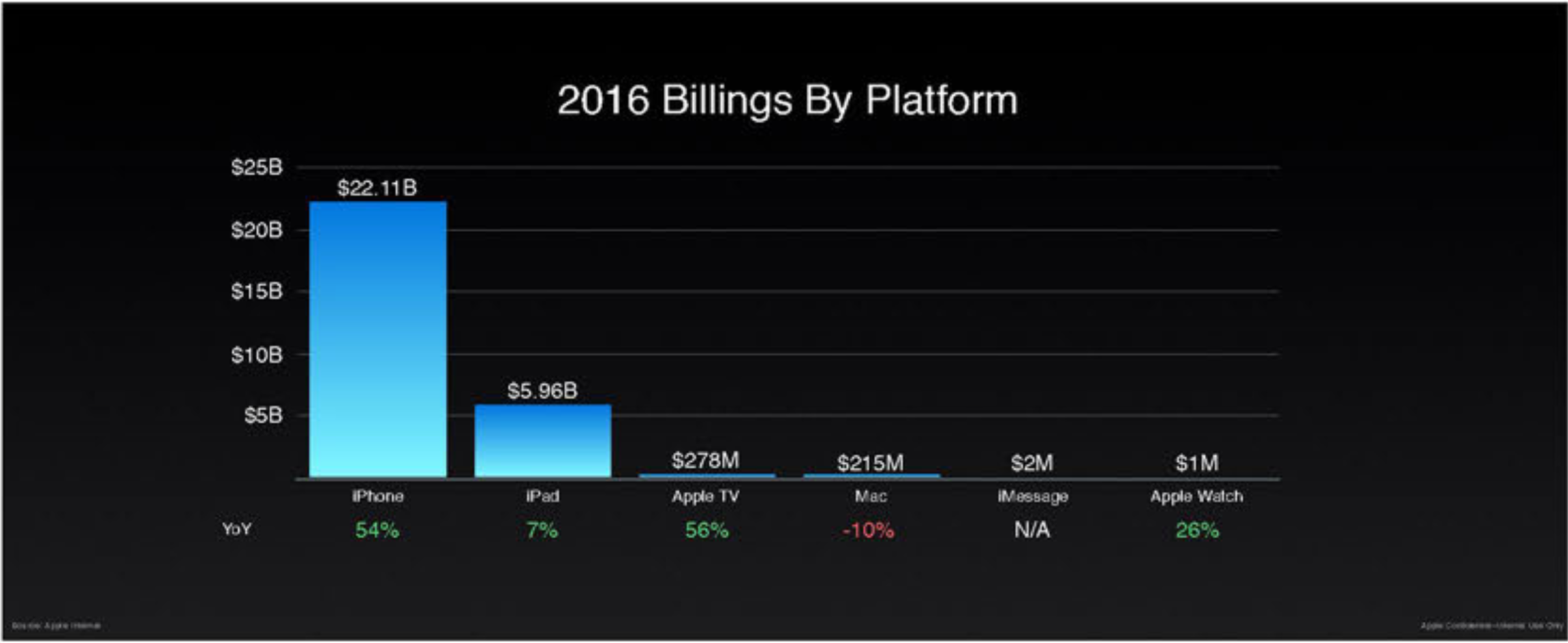

Where did that come from? Apple disclosed the slides above as part of the Epic lawsuit: they show that in 2016, when billings were $28bn, 80% of that was from games, mostly in the US and north-east Asia, and mostly on iPhone. There’s no clear reason to think the proportions have changed much since then, except that China is probably bigger (Apple had only just added support for Alipay in 2016).

So, this is mostly games, and, from other disclosures, over 90% free-to-play. That’s reflected in the top ten publishers. It’s also reflected in the fact that over half of the revenue comes from just 0.5% of the users. If those proportions remain the same, then last year, Apple made $7-8bn in commission revenue from perhaps 5m people spending over $450 a quarter on in-app purchases in games. Apple has started talking a lot about helping you use your iPhone in more healthy ways, but that doesn’t seem to extend to the app store.

20% of users are spending money on the store, and 0.5% of users are 54% of spending

Second, what happens next? Apple will have to allow side-loading and third party app stores, and it will have to allow apps to ask for payment directly. What would that mean?

There are lots of privacy and security arguments about side-loading, and to some extent also third party app stores, but I would argue pretty strongly that this is mostly a waste of effort – that these are not a mainstream consumer behaviour and the dominant route-to-market for most developers will be the default, preloaded app store. That in turn means that even if regulators do force Apple to allow side-loading, they won’t stop there – they will also look at the rules inside the store.

In addition, regulators are not only looking at how an app gets onto the device – they are also looking at the sandbox itself. For example, the EU is looking at Apple’s NFC APIs, and of course there are broader questions about ‘self-preferencing’ of services and products on the device. So, side-loading doesn’t end the argument either way.

Meanwhile, while developers won’t be obliged to use Apple’s payment anymore, that doesn’t mean it will go away – after all it, it will still have lower friction and higher conversion than asking for a credit card. (That prompts the question of whether Apple is obliged to allow side-loaded apps to use it, or to allow other apps to replace Apple as the default for in-app payment.) All things being equal, it’s much easier for big publishers with well-known, trusted brands to ask for a card. So, a lot of the money might stay with Apple, and the money that leaves will mostly go to big companies, and mostly go to game developers. That prompts another question – how much of that money will then be spent on, um, search ads on the App Store?

Part of the complexity here is that US, UK and EU regulators will produce different rules on different timelines. What happens if EU regulators require side-loading but US regulators do not? Will Apple (or Google) have different rules in different places? (Microsoft had to make different versions of Windows.) And note, also, that the EU is moving fastest, but on these numbers was only about 10% of app store billings. What happens when China’s newly aggressive regulators turn their attention to app stores? How many rules will there be?

Third, a slightly more provocative question – if you’re not a shareholder in Apple, Spotify or Epic, why should you care?

Apple’s rules are a structural problem for a small number of businesses that have marginal cost for digital goods – mostly, music and books – and are effectively unable to give Apple 30% of their top line. Ending the current rule would be a big deal here. Conversely, games companies have been able to build a $50bn industry even while giving Apple 30%, though some of them would like the extra cash. Here the issue is not so much Apple’s commission as the business model rules – Stadia is not allowed on the app store at any price, though Roblox is, for reasons no-one understands. Again, this is why a narrow focus on the 30% or side-loading misses the point – regulators are looking at the whole system.

So, are there significant, valuable, mainstream consumer things that can’t happen because of Apple’s rules – not just on that 30%, but on the store and the sandbox? Are there lots of potential Stadias out there being blocked by Apple, or is this just a wealth transfer from Apple to Tencent? Is there an explosion of activity waiting to expand the model far beyond games once the rules are changed?

It’s hard to know in advance. One could argue that the reason all the money is in games is that Apple’s rules have effectively blocked anything other than games and a few other smaller industries (such as online dating) from building a big directly paid software or content model on iOS. For example, people making productivity apps have complained since the beginning about the lack of basic business tools like free trials or upgrade prices. On the other hand, there are very few mainstream consumer successes to point to where Android’s looser rules did enable something that doesn’t exist on iOS. And, of course, companies from Uber to Amazon to Snap or Instagram have built big businesses on the iPhone entirely outside Apple’s rules.

Meanwhile, there are very basic trade-offs between privacy and security, competition, and product design. Apple focuses on the first and third of these, and a lot of current regulatory ideas would deliver the first two while also delivering a system that was baffling and confusing to use. And before the iPhone, mobile apps were a tiny niche industry that delivered none of these. The iPhone app store has been quite good for software developers, after all.

That is, people in tech care deeply about the principles at stake, and some of the arguments can feel very religious. But it’s worth asking whether this is a big deal for a small number of companies, a wealth transfer for a larger number, and mostly irrelevant for most consumers and most consumer tech companies.

* Apple reported ‘over $200bn’ cumulative payments to developers in January 2021 and ‘over $155bn’ in January 2020. Disclosures in the Epic case put Apple’s average commission rate in 2019 at just over 25%, due to the various discounts available.